401k performance

What Would Don Draper Do?

Joined: Jan 2005

Posts: 22,223

Likes: 1

From: Houston

Originally Posted by fuzzy02CLS

Yeah see the trend? Most everyones is down because the market took a bath in January/Feb. Mine is as well almost 3% from Jan 1st.

and yea...it was about 15-17 trading days in january that did it for almost everyone.

Just dial 1911

Joined: May 2004

Posts: 12,144

Likes: 1

From: San Diego, CA

Originally Posted by yunginTL

this year it's barely breaking even, but I have a question.....

I was wondering if I work for a company, that will match 100% up to 3% of my contributions, and 50% of up to the next 2% of contributions. Would it be wise, if I am looking to save for a house, to put the maximum I can afford to save into a 401k, and as a result putting me in a lower tax bracket. Then rolling it over to some type of IRA (which one would I choose?) and withdrawing for first home purchase? I understand 10k is the lifetime limit on withdrawal and I would be subject to income taxes on that but no penalty; is that 10k before or after taxes?

I am only 20 years old, so I do understand that the compounding of interest would be lost. I only have about $1900 saved in there because I only took a 5% salary deduction to take advantage of the free money the company was offering. Would it just be better for me to save for a downpayment via a savings acnt or cd instead of this route?

I was wondering if I work for a company, that will match 100% up to 3% of my contributions, and 50% of up to the next 2% of contributions. Would it be wise, if I am looking to save for a house, to put the maximum I can afford to save into a 401k, and as a result putting me in a lower tax bracket. Then rolling it over to some type of IRA (which one would I choose?) and withdrawing for first home purchase? I understand 10k is the lifetime limit on withdrawal and I would be subject to income taxes on that but no penalty; is that 10k before or after taxes?

I am only 20 years old, so I do understand that the compounding of interest would be lost. I only have about $1900 saved in there because I only took a 5% salary deduction to take advantage of the free money the company was offering. Would it just be better for me to save for a downpayment via a savings acnt or cd instead of this route?

What you need to do is check to see if your company will allow loans. My co. does this. What they do is they let you withdraw a certain amount (I think for us its 50% of your total amount), and you pay yourself back the amount plus a small amount of interest, which also goes back into your account. So, at the end of the loan, you will have more then what you started with. I did a calc a while back just to see how much it would cost to pull out $30K and it was like $350 a month over 10 years. But, if you left your job, it would need to be paid back immediately.

Check with your companies plan administrator to see what your options are...

trill recognize trill

Joined: Nov 2004

Posts: 4,222

Likes: 1

From: htown, tx

Originally Posted by joerockt

Depends. Doing it the way you say wouldn't be wise. 401k's aren't savings accounts. If you withdraw, you'll be heavily taxed on it. Im guessing, but I think its around 20%. This is for a traditional 401k, not sure how a Roth 401k would work.

What you need to do is check to see if your company will allow loans. My co. does this. What they do is they let you withdraw a certain amount (I think for us its 50% of your total amount), and you pay yourself back the amount plus a small amount of interest, which also goes back into your account. So, at the end of the loan, you will have more then what you started with. I did a calc a while back just to see how much it would cost to pull out $30K and it was like $350 a month over 10 years. But, if you left your job, it would need to be paid back immediately.

Check with your companies plan administrator to see what your options are...

What you need to do is check to see if your company will allow loans. My co. does this. What they do is they let you withdraw a certain amount (I think for us its 50% of your total amount), and you pay yourself back the amount plus a small amount of interest, which also goes back into your account. So, at the end of the loan, you will have more then what you started with. I did a calc a while back just to see how much it would cost to pull out $30K and it was like $350 a month over 10 years. But, if you left your job, it would need to be paid back immediately.

Check with your companies plan administrator to see what your options are...

trill recognize trill

Joined: Nov 2004

Posts: 4,222

Likes: 1

From: htown, tx

Originally Posted by joerockt

Looks like you wont be taxed like you said, but you can only use $10K for it...

Originally Posted by yunginTL

this year it's barely breaking even, but I have a question.....

I was wondering if I work for a company, that will match 100% up to 3% of my contributions, and 50% of up to the next 2% of contributions. Would it be wise, if I am looking to save for a house, to put the maximum I can afford to save into a 401k, and as a result putting me in a lower tax bracket. Then rolling it over to some type of IRA (which one would I choose?) and withdrawing for first home purchase? I understand 10k is the lifetime limit on withdrawal and I would be subject to income taxes on that but no penalty; is that 10k before or after taxes?

I am only 20 years old, so I do understand that the compounding of interest would be lost. I only have about $1900 saved in there because I only took a 5% salary deduction to take advantage of the free money the company was offering. Would it just be better for me to save for a downpayment via a savings acnt or cd instead of this route?

I was wondering if I work for a company, that will match 100% up to 3% of my contributions, and 50% of up to the next 2% of contributions. Would it be wise, if I am looking to save for a house, to put the maximum I can afford to save into a 401k, and as a result putting me in a lower tax bracket. Then rolling it over to some type of IRA (which one would I choose?) and withdrawing for first home purchase? I understand 10k is the lifetime limit on withdrawal and I would be subject to income taxes on that but no penalty; is that 10k before or after taxes?

I am only 20 years old, so I do understand that the compounding of interest would be lost. I only have about $1900 saved in there because I only took a 5% salary deduction to take advantage of the free money the company was offering. Would it just be better for me to save for a downpayment via a savings acnt or cd instead of this route?

I used a part of my 401K to pay for my condo. It worked out really well. You are allowed to use up to 50% tax free. And you pay the loan back to yourself. I know a lot of people that went this route to get to a favorable rate. You have 15 years to repay the loan or make larger payments and pay it off faster.

With that said, it is always best to not touch your 401K if you can avoid it. Most of us are not luckly to now have need for the money. A loan is OK, withdrawal is not.

Originally Posted by joerockt

Looks like you wont be taxed like you said, but you can only use $10K for it...

Just dial 1911

Joined: May 2004

Posts: 12,144

Likes: 1

From: San Diego, CA

Originally Posted by RaviNJCLs

For a first time home buyer you are allowed up to 50% of your vested 401K without having to pay taxes on it unless you decide to use it as a withdrawal.

Originally Posted by joerockt

Not what I read. It said the limit was $10K. Dont have the link anymore though...

I just googled it.

I'm at -3% so far this year, but the past two months have been getting me back in the game with +5% gains, up from -8% from Jan-March.

^ And yeah, my condo, not so much either.

^ And yeah, my condo, not so much either.

Registered but harmless

Joined: Aug 2005

Posts: 14,889

Likes: 1,164

From: Los Angeles, CA

Update: UP 3.1% YTD, but DOWN 0.3% overall for past 12 months.

However, I've got 20 years to turn any negative into a positive, or keep it positive, since I'm up overall since inception.

However, I've got 20 years to turn any negative into a positive, or keep it positive, since I'm up overall since inception.

)

)

Advanced

Joined: Feb 2005

Posts: 79

Likes: 0

From: New Jersey

YTD -5.76%

I'm fairly aggressive.

Out of the funds that are available, majority are in the red (-3% to -11% w/ a couple exceptions at -16% and -28% YTD)

3 funds are doing well:

2 REIT funds at ~9% YTD

1 DOW/AIG Commodities TR Index Fund @ ~17% YTD.

I guess I could be doing better.

I'm fairly aggressive.

Out of the funds that are available, majority are in the red (-3% to -11% w/ a couple exceptions at -16% and -28% YTD)

3 funds are doing well:

2 REIT funds at ~9% YTD

1 DOW/AIG Commodities TR Index Fund @ ~17% YTD.

I guess I could be doing better.

Thread Starter

Make MyTL Great Again

Joined: Nov 2004

Posts: 1,686

Likes: 5

From: Dunellen, NJ

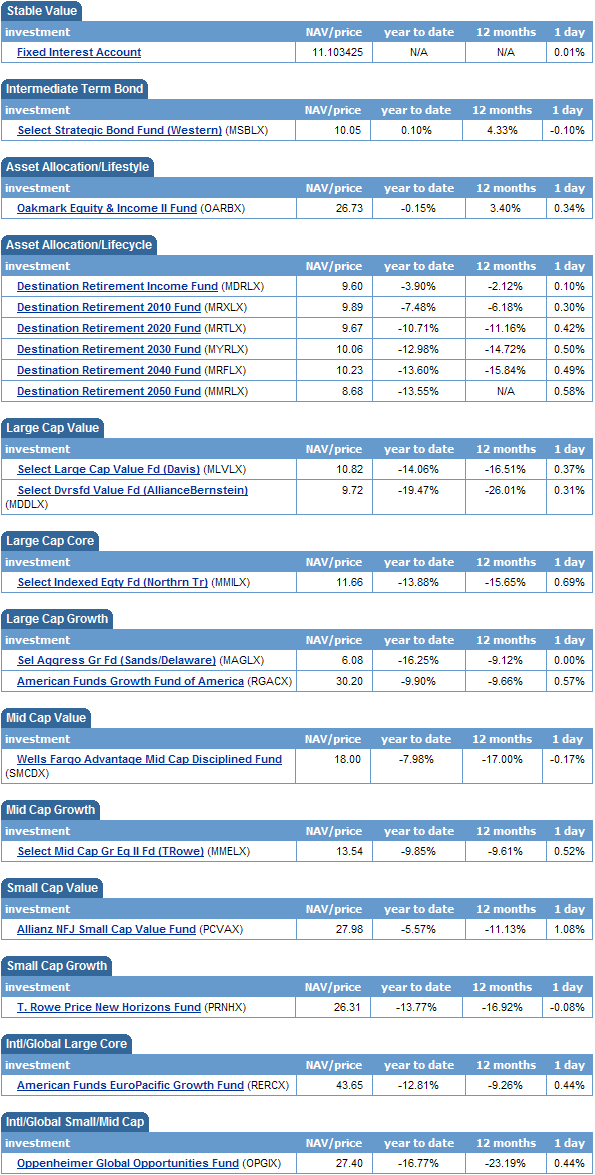

I love it. My 401k had gotten up to ~1-2% positive for the year and now it sucks big time again:

Since the beginning of this year down -12.62% overall!

Code:

variable investment ::::::::::: year to date : 12 months AmerFunds EuroPacific Gr Fund :: -12.81% ::::: -9.26% American Fds Grth Fnd America :: -9.90% p::::: -9.66% Oppenheimer Global Opport Fund : -16.77% ::::: -23.19% Sel Aggr Gr Fd (Sands/Delawre) : -16.25% ::::: -9.12% Sel Dvrsfd Val Fd(AllncBrnstn) : -19.47% ::::: -26.01% T.Rowe Price New Horizons Fund : -13.77% ::::: -16.92% Allianz NFJ Small Cap Value Fu : -5.57% :p:::: -11.13%

Registered but harmless

Joined: Aug 2005

Posts: 14,889

Likes: 1,164

From: Los Angeles, CA

Originally Posted by AdamNJ

I have some great plan options to choose from. Which negative is the best?

Yes, I do know how you feel, though.

Yes, I do know how you feel, though.Look at the 5-year number and try to ignore the "YTD" and "12 month" numbers.

I started a 401K when everyone was complaining about how much their 401Ks dropped 20%+ in 2001, etc. Everything went upwards from there (well, until 2006

).

).

gets all the crazy chicks

Joined: May 2007

Posts: 300

Likes: 0

From: Dirty Jersey

I need to check on my 401k funds (sadly haven't checked it in 2 years, not sure if I even allocated it to a particular fund) but I'm glad I never got around to allocating my IRA funds..maybe now's a good time to do it, with the market in the crapper and all.

What Would Don Draper Do?

Joined: Jan 2005

Posts: 22,223

Likes: 1

From: Houston

Originally Posted by AdamNJ

I love it. My 401k had gotten up to ~1-2% positive for the year and now it sucks big time again:

Since the beginning of this year down -12.62% overall!

Code:

variable investment ::::::::::: year to date : 12 months AmerFunds EuroPacific Gr Fund :: -12.81% ::::: -9.26% American Fds Grth Fnd America :: -9.90% p::::: -9.66% Oppenheimer Global Opport Fund : -16.77% ::::: -23.19% Sel Aggr Gr Fd (Sands/Delawre) : -16.25% ::::: -9.12% Sel Dvrsfd Val Fd(AllncBrnstn) : -19.47% ::::: -26.01% T.Rowe Price New Horizons Fund : -13.77% ::::: -16.92% Allianz NFJ Small Cap Value Fu : -5.57% :p:::: -11.13%

i'm back down to -12%.