When you click on links to various merchants on this site and make a purchase, this can result in this site earning a commission. Affiliate programs and affiliations include, but are not limited to, the eBay Partner Network.

Model 3 production on track to achieve previously announced targets

Expecting positive Model 3 gross margin in Q4; targeting 25% margin in 2018

Deliveries grew 53% compared to Q2�16 in flat luxury vehicle market

Projecting Model S and Model X deliveries to increase in 2H�17 vs 1H�17

Q2 Automotive gross margin at 27.9% GAAP and 25.0% non-GAAP

Q2 GAAP loss from operations improved sequentially, two quarters in a row

More than $3 billion cash on-hand at the end of Q2

On July 28, 2017, we started delivering the �even more affordable car� from our original Master Plan. This was a huge milestone for Tesla and is very exciting for our entire team.

Orders for Model S and Model X have also been increasing, both leading up to and following the Model 3 handover event. In July, our weekly net order rate for these vehicles was about 15% higher than our Q2 average weekly order rate.

In addition, although too early to draw strong conclusions, we are seeing an even further increase in net Model S orders since the July 28th event. This growing demand gives us even more reason to expect increased deliveries of Model S and Model X in the second half of this year.

In addition to the increased orders for Model S and Model X, customer response to Model 3 has been overwhelming. Since the handover event last week, we are averaging over 1,800 net Model 3 reservations per day.

Deliveries to non-employees will begin in Q4

Our first production vehicles are pre-configured with rear-wheel drive, a long-range battery starting at $44,000, with premium upgrades for an additional $5,000. This vehicle will offer a range of 310 miles and a 0-60 mph time of 5.1 seconds. The standard Model 3, starting at $35,000 with 220 miles of range and a 0-60 mph time of 5.6 seconds, should be available in the U.S. in November. Dual Motor All-Wheel Drive configurations will be available in the U.S. early next year. International Model 3 deliveries will begin in late 2018, contingent upon regulatory approvals, starting with left-hand drive markets, followed by right-hand drive markets in 2019.

Based on our preparedness at this time, we are confident we can produce just over 1,500 vehicles in Q3, and achieve a run rate of 5,000 vehicles per week by the end of 2017. We also continue to plan on increasing Model 3 production to 10,000 vehicles per week at some point in 2018.

Automotive revenue grew 93% as compared to Q2 2016 largely due to 53% growth in total vehicle deliveries, and a smaller percentage of vehicles sold with residual value risk that were subject to lease accounting.

About 19% of Q2 deliveries were subject to lease accounting, down from about 25% in Q1, as we retained residual risk on fewer vehicle deliveries. When we do retain residual risk through a Resale Value Guarantee, or direct or indirect leasing, our vehicles are holding value better than estimated. Thus, we expect to be break even when re-selling them.

In line with our guidance, Q2 non-GAAP automotive gross margin was 25.0%, representing a sequential decline of about 285 basis points primarily due to the absence of the one-time benefit of Autopilot software recognized in Q1 and fluctuations in product mix.

Total Q2 operating expenses declined sequentially primarily due to the absence of $67 million of non-recurring charges related to acquisitions that were recognized in Q1.

GAAP and non-GAAP loss from operations improved in Q2 as compared to Q1 due to lower operating expenses, despite increased costs related to the launch of Model 3.

OUTLOOK

In addition to the 2017 Model 3 production guidance provided above, we expect Model S and Model X deliveries to increase in the second half of 2017, as compared to the first half of the year.

Several factors will influence our non-GAAP automotive gross margin for the rest of this year. The combined non-GAAP gross margin for Model S and Model X in Q3 will decline slightly from Q2, driven primarily by mix shift. Additionally, during the initial phase of the Model 3 ramp in Q3, the volume produced will be tiny relative to the installed production capacity. As a result, Model 3 gross margin in Q3 will be temporarily impacted by the excessive allocation of labor and overhead costs and depreciation over this tiny volume. In the absence of these one-time elevated cost allocations, Model 3 gross margin in Q3 would already be positive, resulting in a positive cash contribution. As capacity utilization improves, Model 3 non-GAAP gross margin is expected to be positive in Q4, and should improve rapidly in 2018 to our target of 25%. Consequently, we expect non-GAAP automotive gross margin to temporarily dip below 20% in Q3, before recovering in Q4 and beyond.

For the second half of 2017, we expect strong improvement in operating leverage as revenue should significantly increase in the second half of the year as compared to the first half, while operating expenses should remain essentially flat. Capital expenditures should be about $2 billion during the second half of 2017, as we make milestone-based payments for Model 3 equipment, continue with Gigafactory 1 construction, and expand our Supercharger, store, delivery hub, and service networks.

While delivering the first Model 3 cars was a major company milestone, we are now focused on the critical steps to ramp Model 3 production. We remain confident in our plans and look forward to the upcoming unveiling of the next exciting addition to our portfolio of electric vehicles � Semi Truck.

Tesla earnings: Model 3 production, demand under the microscope

Oct. 31, 2017

Through delays, recalls, and wildly optimistic projections, Wall Street has stuck with Tesla Inc. shares, which have gained three times as much as the benchmark this year.

Tesla is expected to report a third-quarter loss after the bell Wednesday, but that too is likely to be brushed off.

All eyes will be on whether the company can make a good case that it has worked out all the kinks with the production of the Model 3, its first electric car aimed at the masses.

Moreover, if Tesla is able to show that demand for the Model 3 continues to be strong and that the market for its luxury vehicles is not reaching saturation, investors will look past the quarterly numbers, said Bill Selesky, an analyst with Argus Research.

Production shortfalls could become more of a concern in 12 to 18 months, but right now investors are more interested in hearing from the demand side.

Here�s what to expect from Tesla�s earnings:

Earnings: Analysts surveyed by FactSet expect Tesla to report an adjusted loss of $2.31 a share in the quarter, versus adjusted earnings of 71 cents a share in the third quarter of 2016. Tesla has posted three consecutive quarterly losses.

Estimize, a crowdsourcing platform that gathers estimates from Wall Street analysts as well as buy-side analysts, hedge-fund managers, company executives, academics and others, has projected an adjusted loss of $2.25 a share.

Revenue: The FactSet revenue consensus is $2.95 billion, which would be down from $2.30 billion in the same quarter last year. Estimize is projecting revenue of $2.95 billion.

Other issues: Despite the share run so far this year, this has been a humbling month for Tesla. The stock is down 5.9% in October, an aftershock of news earlier in the month that Tesla delivered only a fraction of the Model 3 sedans that Chief Executive Elon Musk had promised.

At the time, Tesla pinned the slower-than-expected Model 3 production ramp to �bottlenecks� but reiterated there were no fundamental issues with production or the supply chain and that it knew what had to be fixed.

Tesla delivered 220 and produced 260 Model 3s in the third quarter. Musk had said that he would expect to see production increase to 1,500 Model 3s by September, with plans to dial that up to 5,000 by the end of the year and 10,000 a week by the end of 2018.

Tesla will need to produce anywhere from 1,200 to 1,700 Model 3 vehicles a day depending on how long it wants its work week to be to clear the Model 3 backlog (Tesla has said preorders hover around 450,000) and book the associated revenue in the span of 12 months, said Rebecca Lindland, an analyst with Cox Automotive.

�This will be extremely difficult unless they start to get production really rolling,� she said. �A much more likely scenario is two full years to clear the backlog, but will people at the back of the line wait an additional year? I�ll be curious to see what leaks about the abandonment rate of the Model 3 deposits. I know I�m having second thoughts.�

- Reports loss of $2.92 vs estimates for loss of $2.31 per share (FactSet) ; loss of $2.25 per share (Estimize)

- Revenue of $2.98 billion vs estimates for revenue of $2.95 billion (FactSet, Estimize)

I guess this bigger than expected loss explains why Tesla was firing all those people at Tesla and SolarCity recently. Cutting costs.

Pushing back Model 3's 5,000 unit per week production run rate back almost 3 months to late Q1 2018 vs previous goal of Q4 2017.

Tesla shares down 5% after reporting bigger than expected loss of $2.92 per share

Tesla struggled in the third-quarter with "production bottlenecks" on its Model 3 sedan.

Nov. 1, 2017

Tesla shares fell Wednesday after the company posted a wider-than-expected loss as it spent heavily to ramp up production of its Model 3, its first mass market electric sedan.

Complications with Tesla's manufacturing processes have slowed production of the Model 3, a car widely considered key to Tesla's future success. Hopes for the Model 3 have helped propel Tesla's stock so far this year.

Tesla said in a letter to shareholders it expects to achieve a production rate of 5,000 Model 3 cars per week by late in the first quarter of 2018. Previously, the company had said it hoped to achieve that number by the end of 2017.

Here's how the company did compared with what Wall Street expected:

Loss per share of $2.92 vs. $2.29 expected according to Thomson Reuters

Revenue of $2.98 billion vs. $2.95 billion expected according to Thomson Reuters

Tesla said it had record net orders and deliveries of its Model S and Model X in the third quarter, and said its production rate of the Model 3 is steadily increasing.

The company said it has a cash balance of $3.5 billion entering the fourth quarter.

- Record Model S and Model X net orders and deliveries in Q3 2017

- About 100,000 Model S and X deliveries projected for 2017

- Model 3 production steadily increasing

- Cash balance of $3.5B entering Q4 2017

While we continue to make significant progress each week in fixing Model 3 bottlenecks, the nature of manufacturing challenges during a ramp such as this makes it difficult to predict exactly how long it will take for all bottlenecks to be cleared or when new ones will appear. Based on what we know now, we currently expect to achieve a production rate of 5,000 Model 3 vehicles per week by late Q1 2018, recognizing that our production growth rate is like a stepped exponential, so there can be large forward jumps from one week to the next. We will provide an update when we announce Q4 production and delivery numbers in the first few days of January. With respect to the timing for producing 10,000 units per week, it has always been our intention to implement that capacity addition after we have achieved a 5,000 per week run rate. That will enable us to make the next generation of automation even better while making our capex spend significantly more efficient.

Demand for Model 3 is not going to be a constraint for quite a long time. The global net reservations for Model 3 continued to grow significantly in Q3.

In Q3, we delivered 25,915 Model S and Model X vehicles and 222 Model 3 vehicles, for a total of 26,137 deliveries. Combined Model S and Model X deliveries in Q3 grew 18% globally compared to Q2 and 4.5% versus the same quarter one year ago. Consequently, both Model S and Model X gained further market share in the US luxury vehicle market. In addition, our used vehicle sales more than doubled from the prior quarter.

Model S and X combined net orders in Q3 also hit an all-time record in our North American, European and Asian markets individually, driven primarily by increased awareness of Tesla from the Model 3 launch and the addition of new stores internationally.

Revenue & Gross Margin

- Automotive revenue grew 10% as compared to Q3 2016 mainly due to a 4.5% increase in Model S and Model X volumes. ZEV credit sales were less than $1 million in Q3 as compared to $100 million in Q2 and $139 million in Q3 last year.

- Approximately 21% of Q3 deliveries were subject to lease accounting, which is roughly consistent with Q2. Initially for Model 3, we will not be offering a lease financing option, which will result inupfront revenue recognition of the vehicle and improved cash flows from Model 3 deliveries.

- Non-GAAP automotive gross margin temporarily declined to 18.7%, which was in line with our expectations. The gross margin declined primarily because of a significant increase in Model 3 manufacturing costs to support the limited initial level of production.

- Model S and Model X gross margin declined from Q2 primarily due to one-time price adjustments for discontinued trims and unfavorable trim mix. Numerous actions to improve Model S and Model X gross margin are underway. Consequently, we expect Model S and Model X gross margin to improve in upcoming quarters.

Cash Flow and Liquidity

- Cash outflow from operating activities during Q3 benefited from the management of working capital. Lower inventory of new and used vehicles and higher customer deposits improved working capital, with a partial offset due to higher accounts receivables.

- In August, we completed the issuance of $1.8 billion of Senior Notes due 2025 at an interest rate of 5.3%. We also used cash to terminate a revolving credit facility by repaying the outstanding balance of $325 million. At the end of Q3, our gross cash balance increased to $3.5 billion.

- Capital expenditures were $1.1 billion in Q3. The majority of capital expenditures were attributable to Model 3 and Gigafactory 1 production capacity increases.

OUTLOOK

Based on the recent acceleration in order growth, we now expect that Model S and Model X are on pace for about 100,000 deliveries in 2017, an increase of 30% compared to 2016. Notwithstanding these increased deliveries, we plan to produce about 10% fewer Model S and Model X in Q4 compared to Q3 because of the reallocation of some of the manufacturing workforce towards Model 3 production. As a result, inventory level of finished Model S and X vehicles should continue to decline.

We expect Model 3 non-GAAP gross margin to reach breakeven by end of Q4, because of increased capacity utilization, and it should improve rapidly in 2018 to our target of 25%. Our recent production challenges may affect short-term costs, but they have no impact on our 25% gross margin target, since there has been no change to our projections for material, labor and overhead costs per vehicle.

Due to a higher mix of temporarily lower margin Model 3 deliveries in Q4 compared to Q3, we expect non-GAAP automotive gross margin to temporarily decline slightly in Q4 to about 15% and then recover starting in Q1. Gross profit is expected to grow more than operating costs in Q4 compared to Q3, while operating costs are expected to be flat to up slightly in Q4. Between cash on hand, future cash flows and available lines of credit, we believe that we are well capitalized to accommodate the revised ramp of Model 3 production to 5,000 per week. Upon achieving this production level, we expect to generate significant cash flows from operating activities.

Capital expenditures are expected to be approximately $1 billion in Q4, driven largely by milestone payments on Model 3 production equipment, as well as Gigafactory 1, and further expansion of stores, service centers, delivery hubs and the Supercharger network.

Tesla earnings: Model 3 is still the issue investors care most about

Feb 7, 2018

Tesla is scheduled to report fourth-quarter results after the bell on Wednesday, and investors are sure to parse every word the company utters about the Model 3 production ramp.

Meanwhile, its stock performance continues to outperform benchmarks and competitors, even though the company is expected to report a wider loss for the quarter.

Earnings: Analysts surveyed by FactSet expect Tesla to report an adjusted loss of $3.11 a share in the quarter, compared with an adjusted loss of 69 cents a share in the fourth quarter of 2016.

Estimize, a crowdsourcing platform that gathers estimates from Wall Street analysts as well as buy-side analysts, hedge-fund managers, company executives, academics and others, has also projected an adjusted loss of $3.11 a share.

Revenue: The FactSet revenue consensus is $3.3 billion, which would be up from $2.3 billion in the same quarter last year. Estimize has the same consensus.

Reports non-GAAP loss of $3.04 per share vs expected loss of $3.11 (FactSet, Estimize) . . . GAAP loss is $4.01

Revenue of $3.29 billion vs expectations for $3.3 billion (FactSet, Estimize)

Free cash flow: -$276.8 million vs expectations for -$958 million. . . . much much better than expected

Cash balance of $3.4B entering Q1 2018

2018 revenue growth expected to significantly exceed 2017 growth

At some point in 2018, we expect to begin generating positive quarterly operating income on a sustained basis. With the planned ramp of both Model 3 and our energy storage products, our rate of revenue growth this year is poised to significantly exceed last years growth rate. The launch of Model 3 is what Tesla had been building towards from day one. We incorporated all the learnings from the development and production of Roadster, Model S, and Model X to create the world’s first mass market electric vehicle that is priced on par with its gasoline-powered equivalents – even without incentives. Now we are ramping up production significantly, and as we look ahead in 2018, we are on the cusp of a step change in the world’s transition to sustainability.

We continue to target weekly Model 3 production rates of 2,500 by the end of Q1 and 5,000 by the end of Q2. It is important to note that while these are the levels we are focused on hitting and we have plans in place to achieve them, our prior experience on the Model 3 ramp has demonstrated the difficulty of accurately forecasting specific production rates at specific points in time. What we can say with confidence is that we are taking many actions to systematically address bottlenecks and add capacity in places like the battery module line where we have experienced constraints, and these actions should result in our production rate significantly increasing during the rest of Q1 and through Q2.

As we shared previously, in order to incorporate our learnings and be capital efficient, we intend to start adding enough capacity to get to a 10,000 unit weekly rate for Model 3 once we have first hit the 5,000 per week milestone. Despite the delays that we experienced in our production ramp, Model 3 net reservations remained stable in Q4. In recent weeks, they have continued to grow as Model 3 has arrived in select Tesla stores and received numerous positive reviews, including Automobile Magazine’s 2018 Design of the Year award.

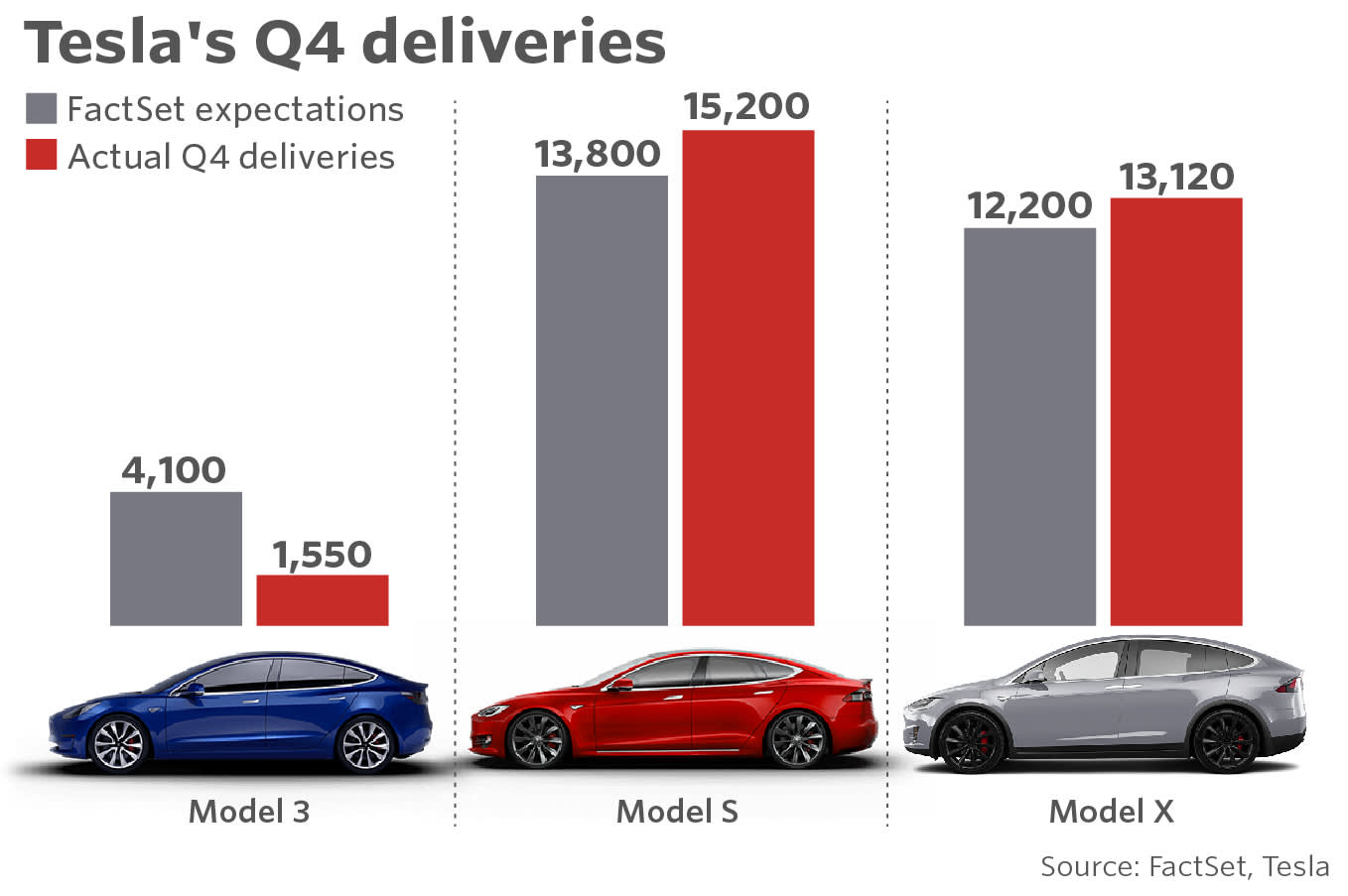

In Q4, we delivered 28,425 Model S and Model X vehicles and 1,542 Model 3 vehicles, totaling 29,967 deliveries. Combined Model S and Model X deliveries in Q4 grew 10% globally compared to our prior record in Q3, and they grew 28% compared to Q4 2016. As we indicated heading into Q4, production of Model S and Model X during the quarter was limited to 22,137 vehicles due to reallocation of some of the manufacturing resources to Model 3 production. This enabled us to reduce our finished-goods inventory to the lowest level in about 18 months.

Combined Model S and Model X net orders in Q4 were just shy of Q3’s all-time high. Importantly, combined orders for Model S and Model X grew significantly in 2017 compared to 2016. There had initially been concerns about whether Model 3 would cannibalize Model S and Model X. It seems the opposite is true. In stores where Model 3 is on display, customer foot traffic has increased considerably and orders for Model S and Model X have in fact increased. There has been an even bigger increase in solar and Powerwall sales.

Automotive revenue in Q4 increased by 36% over Q4 2016, mainly due to 35% growth in vehicle deliveries. For 2017, Automotive revenue was up 52% from 2016. ZEV credit sales in Q4 were $179 million as compared to $20 million in Q4 2016.

GAAP Automotive gross margin improved slightly compared to Q3 to 18.9%. Non-GAAP Automotive gross margin declined to 13.8% in Q4, which was below our expectations. This is more than fully explained by the slower than expected ramp of Model 3. Since Model 3 production was in the early stages of the ramp, allocation of full operating costs and depreciation made its gross margin negative. We are expecting a negative Model 3 gross margin in Q1, while generating positive operating cash flows.

Model S and Model X gross margin in Q4 declined very slightly compared to Q3. This was primarily due to significant reserves booked for fixed assets that are no longer in service. We expect Model S and Model X gross margins to increase in 2018 with improved trim mix and option content, lower cost of acquisition and lower manufacturing costs.

OUTLOOK

2018 will be a transformative year for Tesla, with a high level of operational scaling. As we ramp production of both Model 3 and our energy products while keeping tight control of operating expenses, our quarterly operating income should turn sustainably positive at some point in 2018.

We expect Model S and Model X deliveries to be approximately 100,000 in total, constrained by the supply of cells with the old 18650 form factor. As our sales network continues to expand to new markets in 2018, we believe orders should continue to grow. Withdemand outpacing production, we plan to optimize the options mix in order to maximize gross margin. As stated above, we continue to target a weekly Model 3 production rate of 2,500 by the end of Q1 and 5,000 by the end of Q2. Also, we are focused on achieving our target of 25% gross margin for Model 3 after our production stabilizes at 5,000 cars per week.

Capital expenditures in 2018 are projected to be slightly more than 2017. The majority of the spending will be to support increases in production capacity at Gigafactory 1 and Fremont, and for building stores, service centers, and Superchargers.

Tesla's Plummeting Share Price Shows That Musk Is Running Out Of Time

Mar 26, 2018

. . . . not a single one of my contacts at global automakers is worried about Tesla's Model 3. This is for the simple reason that Tesla simply cannot make this model in volume, and Musk's target of production of 2,500 Model 3s per week by quarter-end is not taken seriously by my contacts in the automotive world, including those at companies that supply components for that model.

Eventually Tesla will make Model 3s in volume say the TSLA bulls, but the bearish argument is summed up in one word: when? The clock is ticking for Tesla owing to the fact that the company issued $1.8 billion in debt last August. With Tesla reporting negative EBITDA for the past two quarters -- and my modeling shows it will be negative again in the first quarter of 2018 -- something's gotta give here.

Issuing straight debt was a colossal mistake by Tesla, and those bonds are now trading at about 92 cents on the dollar; yielding 6.65% versus a coupon of 5.3%. Tesla has convertible bonds expiring in June this year that were issued in 2013 with a 1.5% coupon and a conversion price of $124/share. That was a huge win for the company, and I have no idea why Tesla doesn�t keep issuing converts to its legion of numbers-blind devotees on the buy-side. The only reasonable explanation is that Musk doesn't want to incur further dilution as a current -- and TSLA's largest -- shareholder.

Tesla needs to tap the equity markets for a follow-on offering very soon, but the fall in the value of TSLA shares means that to raise an appropriate amount of money, TSLA will need to offer more shares than it would have a month ago, thus incurring even more dilution. It's a vicious circle, but if Tesla does not raise at least $2 billion, in my opinion, the company will not be able to fund its obligations in 2019.

So, time is of the essence for Tesla and Musk. Elon needs to swallow his male pride and swamp the markets with TSLA shares, which, other things equal, will cause the shares to decline. The alternative is for Tesla to run out of time. The company factored its leases in January, and there simply are no more financial levers to pull. If Tesla does not raise capital in the next three months, I believe it will be increasingly difficult for TSLA to convince its business partners that it is a viable entity.

It may indeed be better to burn out than to fade away, but if you hold TSLA shares you need to prepare yourself for the very real possibility that Tesla will cease to exist within 12 months. Without fresh capital that�s the most likely outcome, in my opinion. It's scary prospect, but with a market valuation of $49 billion -- still not even remotely priced into TSLA shares.

Tesla shares drop to the lowest since April on fatal crash investigation, bearish analyst note

Mar. 27, 2018

Tesla shares fell after the National Transportation Safety Board said it sent investigators to look into a fatal car crash last week in California, according to a post on social media.

A negative analyst call from Citigroup also weighed on the stock, which has been under pressure this past one month.

The NTSB's post on Twitter said: "2 NTSB investigators conducting Field Investigation for fatal March 23, 2018, crash of a Tesla near Mountain View, CA. Unclear if automated control system was active at time of crash. Issues examined include: post-crash fire, steps to make vehicle safe for removal from scene."

Citi Research said Tuesday that its analysis of the company's Model 3 competition points to near-term risk for the stock.

"We open a 90-day downside catalyst watch on Tesla shares," the report said.

Tesla shares declined 5.8 percent Tuesday to their lowest price since April of last year. The stock is down 18 percent in the last one month.

Tesla's Weak Financials Are Finally Being Exposed In Its Stock Price

Mar 27, 2018

The continued delays in Model 3 production have stretched Tesla's automotive resources, but that's only half the point. Tesla Inc. also has to service the debt associated with its money-losing SolarCity subsidiary. When Steve Jobs changed his company�s name from Apple Computer to Apple Inc. on January 9, 2007, that was a pretty good buy point for AAPL shares, to say the least. When Musk, the largest shareholder of both TSLA and SCTY, changed his company's name from Tesla Motors to Tesla Inc. in January 2017, that was the beginning of the end of for Tesla as a public company, in my opinion.

TSLA bulls can point to the company's $3.367 billion of cash on its balance sheet as of 12/31/2017, but the markets are forward-looking mechanisms that can see through the moment-in-time figures on a balance sheet. Tesla's unique sales model means that the company generates relatively few receivables, but that also means that the steady flow of cash that other automakers receive as payments from their dealers doesn't exist at Tesla.

So, for Tesla to fund its automotive business, it needs to either use debt, equity or continue to generate a high number of deposits. Tesla's customer deposits were $854 million at year-end compared with $686 million at the end of the third quarter of 2017. Again, though, I am not sure that figure, which is presented as a current liability in Tesla's financials, should be viewed a positive or a negative. If Tesla achieves planned production of 2,500 per week units of Model 3 production by quarter-end and 5,000 per week by mid-year, that figure would drop rapidly. Multiple published stories and analyst reports have noted those figures are extremely unlikely to be achieved, however, and thus the process of turning those deposits into badly-needed cash is just not happening rapidly enough at Tesla.

Adding to the well-publicized problems at Tesla's Fremont, CA assembly plant is the issue of the recession -- some would say depression -- gripping the U.S. solar power market. Tesla's SolarCity division deployed 87 MWh of solar generation capacity in the fourth quarter of 2017 versus 201 MWh in the fourth quarter of 2016 and 253 MWh in the fourth quarter of 2015. Tesla has stopped aggressively marketing SolarCity's products to customers and has cut down on leasing, but while these methods control costs they do not address SolarCity�s debt burden.

SolarCity carries a substantial portion of Tesla's debt, and in fact the notes issued in August 2017 technically were issued by SolarCity, not Tesla. Since SCTY is fully consolidated that distinction doesn't really matter, but as per the company's 10-K, the net debt assumed by Tesla in the SolarCity acquisition was $3.4 billion (including both recourse and non-recourse debt.) Musk recused himself from the TSLA-SCTY shareholder votes, but, honestly, putting $3.4 billion of debt from a solar power company onto a car company that has never generated positive cash flow was really stupid.

Tesla�s convertible notes issued in 2013 and 2014 (by what was then Tesla Motors) were a huge success for investors and the company, with infinitesimal coupon rates and conversion prices well below the current stock price. In contrast, SolarCity's converts, now fully guaranteed by Tesla, are well underwater and need to be redeemed soon. TSLA has $230 million in face value of SCTY converts due in November 2018 with a conversion factor of $560/TSLA share. It gets worse next year, as $566 million of old SCTY converts mature in November 2019, and those notes carry a pie-in-the-sky conversion factor of $759/TSLA share. So, that's nearly $800 million of liabilities that will, in all likelihood, need to be settled in cash.

Tesla's 5.3% 2025 notes are trading down again today, and were last quoted at 91.25 cents on the dollar.

Moody's downgrades Tesla credit rating on Model 3 production delays

Mar 27, 2018

Moody's downgraded Tesla's credit ratings Tuesday and changed its outlook to negative from stable, citing "significant shortfall" in the Model 3 production rate and a tight financial situation.

The credit ratings agency also said the electric car maker will likely need to raise more money in the near future to meet its cash needs and maintain its expected pace of expansion.

Moody's lowered its corporate family rating on Tesla to B3 from B2 and downgraded its rating on the company's senior notes to Caa1 from B3. The speculative grade liquidity rating was cut to SGL-4 from SGL-3.

Tesla declined to comment on the Moody's downgrade. S&P has a negative B rating on Tesla and a negative outlook, as of April 2017.

"Tesla's ratings reflect the significant shortfall in the production rate of the company's Model 3 electric vehicle," Moody's said in a release. "Tesla's rating could be lowered further if there are shortfalls from its updated Model 3 production targets."

Elon Musk's electric car company had planned to produce 5,000 Model 3 sedans a week by the end of last year, but has since pushed that goal out by half a year.

The price on Tesla's eight-year junk bond, which matures in 2025, fell to its lowest since it was issued in August. It hit 90.8 cents late Tuesday afternoon just ahead of the Moody's announcement, according to IHS Markit. The yield, which moves inversely to price, rose to 6.91 percent, the data showed.

Tesla raised a more-than-expected $1.8 billion in August for that junk bond offering to fund accelerated production for its Model 3 sedan, despite poor appetite at the time for risky assets.

Traders have been betting heavily against the electric car maker's bonds amid growing worries about the electric car maker's ability to deliver on its production goals. Ninety-nine percent of lendable supply for shorting Tesla's high-yield bond has been used, Sam Pierson, director, securities finance, at IHS Markit said in a Monday note.

Tesla had $3.4 billion in cash and securities at the end of last year, and $1.9 billion through its asset-based lending facility, the Moody's release said. "This liquidity position is not adequate to cover:

1) the approximately $500 million in minimum cash that we estimate Tesla must maintain for normal operations;

2) a 2018 operating cash burn that will approximate $2 billion if Tesla maintains high discretionary capital expenditures to increase capacity; and

3) convertible debt maturities of approximately $1.2 billion through early 2019. These cash needs will likely require Tesla to undertake a near-term capital raise exceeding $2 billion."

"These cash needs will likely require Tesla to undertake a near-term capital raise exceeding $2 billion," Moody's said in the release.

The firestorm surrounding Tesla's creditworthiness intensified late Tuesday as Moody's downgraded Tesla's Corporate Family Rating from B3 to B2. Tesla's bonds sank after the news and were last quoted at 87.7 cents on the dollar. I've been asked many times the last few days how to check Tesla's bond prices; the source is Finra's TRACE system and the link to pricing of Tesla' 5.3% notes due 2025 is here.

Why is there so much pressure on Tesla shares now? The market is eagerly anticipating Tesla's disclosure of first quarter deliveries and production. Tesla discloses this soon after quarter-end, so that means there will be a discovery action early next week. It has been widely reported, and my sources in the auto supply industry confirm, that Tesla's Model 3 production was well below the targeted 2,500 per week level throughout the first quarter. I guess the market is trying to figure out "how bad is bad" when it comes to Model 3 production, but as I mentioned in my column yesterday, I think SolarCity's massive operational slowdown and intimidating debt burden are pressuring Tesla's balance sheet as much as its automotive operations are.

What can Musk do? When the solution to having too much debt is to issue more debt, that's just not a good solution. With Tesla�s 2025 notes trading at what bond traders measure as a YTW (the annual rate of return to the earliest call date) of 7.18% it is becoming economically prohibitive for Tesla to issue more straight debt. If the company tried, the YTW on the existing bonds would likely rise to a level well in excess of that 7.18% figure. There is a diminishing return from issuing additional debt owing to the additional default risk it adds.

So, Elon needs to sell stock. I said that in my Forbes column Monday, I said that in my Forbes column Tuesday, and I am saying that again today. Will he do it? I don�t know. To raise $2 billion at TSLA's current stock price would entail the issuance of 7.54 million shares, an implied dilution of 4.5%. Of course, such an offering would signal to the stock market what the bond market and I have been saying -- this company is in severe financial distress -- and likely send TSLA shares lower. Still, 5% dilution seems small in the grand scheme of Musk's plans for global automotive domination. I cannot understand why he has not yet greenlighted such a move.

PALO ALTO, Calif., April 03, 2018 (GLOBE NEWSWIRE) -- Q1 production totaled 34,494 vehicles, a 40% increase from Q4 and by far the most productive quarter in Tesla history. 24,728 were Model S and Model X, and 9,766 were Model 3. The Model 3 output increased exponentially, representing a fourfold increase over last quarter. This is the fastest growth of any automotive company in the modern era. If this rate of growth continues, it will exceed even that of Ford and the Model T.

We were able to double the weekly Model 3 production rate during the quarter by rapidly addressing production and supply chain bottlenecks, including several short factory shutdowns to upgrade equipment.

In the past seven days, Tesla produced 2,020 Model 3 vehicles. In the next seven days, we expect to produce 2,000 Model S and X vehicles and 2,000 Model 3 vehicles. It is a testament to the ability of the Tesla production team that Model 3 volume now exceeds Model S and Model X combined. What took our team five years for S/X, took only nine months for Model 3.

Given the progress made thus far and upcoming actions for further capacity improvement, we expect that the Model 3 production rate will climb rapidly through Q2. Tesla continues to target a production rate of approximately 5,000 units per week in about three months, laying the groundwork for Q3 to have the long-sought ideal combination of high volume, good gross margin and strong positive operating cash flow. As a result, Tesla does not require an equity or debt raise this year, apart from standard credit lines.

Q1 deliveries totaled 29,980 vehicles, of which 11,730 were Model S, 10,070 were Model X, and 8,180 were Model 3. Net orders for Model S and X were at an all-time Q1 record, and demand remains very strong. Model S and X customer vehicles in transit were high. 4,060 Model S and X vehicles were in transit to customers at the end of Q1, which was 68% higher than at the end of Q4 2017. An additional 2,040 Model 3 vehicles were also in transit to customers. These vehicles will be delivered in early Q2 2018, which keeps us on track for our full-year 2018 Model S and X delivery guidance.

Finally, we would like to share two additional points about Model 3:

The quality of Model 3 coming out of production is at the highest level we have seen across all our products. This is reflected in the overwhelming delight experienced by our customers with their Model 3's. Our initial customer satisfaction score for Model 3 quality is above 93%, which is the highest score in Tesla's history.

Net Model 3 reservations remained stable through Q1. The reasons for order cancellation are almost entirely due to delays in production in general and delays in availability of certain planned options, particularly dual motor AWD and the smaller battery pack. As described above, owner happiness with the product is extremely high.

We would like to thank our customers, suppliers and investors for their continued patience and belief in Tesla.

Our delivery count should be viewed as slightly conservative, as we only count a car as delivered if it is transferred to the customer and all paperwork is correct. Final numbers could vary by up to 0.5%. Tesla vehicle deliveries represent only one measure of the company's financial performance and should not be relied on as an indicator of quarterly financial results, which depend on a variety of factors, including the cost of sales, foreign exchange movements and mix of directly leased vehicles.

Tesla says no need for capital raise as Model 3 output rises

April 3, 2018

(Reuters) - Tesla Inc quashed any speculation it might need to raise more capital this year on Tuesday, driving the company�s battered shares higher as it announced it built 2,020 of its cheaper Model 3 sedans in the last seven days of March.

The company, damaged in the past week by speculation over its finances and a car crash in California, said it would produce nearly the same number of the Model 3 in the next week and would see output climb rapidly through the second quarter.

�Tesla continues to target a production rate of approximately 5,000 units per week in about three months, laying the groundwork for Q3 to have the long-sought ideal combination of high volume, good gross margin and strong positive operating cash flow,� it said.

�As a result, Tesla does not require an equity or debt raise this year, apart from standard credit lines.�

The production numbers, short of Tesla�s own target of 2,500 per week for the end of March, are far above the 793 Model 3s built in the final week of last year.

Quickly ramping up Model 3 production is crucial for the Silicon Valley electric vehicle maker, whose profitability depends on the cheaper sedan. Tesla says it has about 500,000 advance reservations from customers for the car.

Analysts from brokerage Evercore ISI said a run-rate of 2,000 per week, while short of the 2,500 target, was better than most on Wall Street had expected and clearly showed progress versus where the company was at the start of the year.

�We were able to double the weekly Model 3 production rate during the quarter by rapidly addressing production and supply chain bottlenecks, including several short factory shutdowns to upgrade equipment,� Tesla said in the filing.

Tesla stock drops as Elon Musk gives bizarre earnings call

Tesla stock dropped more than 5% in after-hours trading as executives cut off Wall Street analysts in an earnings call dubbing their questions on Model 3 gross margins "boring."

CEO Elon Musk took several questions, instead, from Gali Russell, a 25-year-old retail investor in Tesla and Youtuber.

Elon Musk expands Tesla stake after jumping on short sellers

May 7, 2018

Elon Musk did more than just talk smack to short sellers in tweets. On Monday, Musk, already the company’s largest shareholder, expanded his own stake in Tesla.

The chief executive officer of the electric auto maker bought about $9.85 million worth of Tesla shares, his biggest purchase since March 2017, according to a regulatory filing.

Musk has now grown his stake to near 20%, according to data compiled by Bloomberg.

Musk last week promised to “burn” those betting against the company, which hasn’t earned a yearly profit in its 15-year history and who analysts believe will continue to “bleed cash.”

Short interest in the stock increased by nearly 400,000 shares on May 3, the day after the earnings report, bringing the total to more than 40 million shares for the first time in Tesla’s history, said S3 Partners’ Ihor Dusaniwsky, according to Barron’s.

“The sheer magnitude of short carnage will be unreal,” Musk tweeted, sharing the Barron’s article that also said Tesla shorts are facing dwindling supplies. “If you’re short, I suggest tiptoeing quietly to the exit…,” he said.

Tesla stock rose nearly 3% Monday. It trades down about 2.8% so far in 2018 and is off 5.7% over the past year.

Tesla’s ‘cash bleed’ will likely double, analyst says

May 7 2018

Tesla Inc.’s “cash bleed” will likely double in the second quarter as the Silicon Valley car maker attempts to ramp up production of its Model 3 sedan, analysts at CreditSights said Monday.

Liquidity at Tesla will remain “tight” before its cash situation improves in the second half of the year, said the analysts, who analyze company debt. Tesla is banking on a steady production rate for the Model 3 and product turnover in the second half to rebuild its cash balance, they said.

“Execution on its high-volume Model 3 production plan remains critical to Tesla’s ability to successfully and economically raise capital for future product launches and support its high equity valuations,” CreditSights analysts Hitin Anand and Brendan Keevan wrote in commentary.

Tesla has raised about $9.23 billion since 2017, including $1.8 billion in its first-ever pure bond sale last August.

The 5.300% notes, which mature in 2025, last traded at 87.625 cents on the dollar to yield 7.541%, according to trading platform MarketAxess. On a spread basis, they were trading at 459 basis points above comparable Treasurys.

The CreditSights analysts kept the equivalent of a sell rating on the Tesla bonds, saying the risk-reward on the bonds is “still not attractive” given subordination risk, execution risk beyond the Model 3, and need for “continuous capital to support its growth ambitions.”

Musk has said Tesla would not tap capital markets in the near future, but the CreditSights analysts joined many on Wall Street who believe it will need to at some point this year. Capital needs at Tesla “remain high and consistent,” they wrote.

“Further capital raise for Model 3 possibly can be avoided, but Tesla will most certainly need debt/equity funding for future growth projects,” the CreditSights analysts said. Tesla’s projects include the Model Y, believed to be a compact SUV, expected for 2020.

Holy fuck, Elon is predicting $100/kwh batteries by the end of the year! A Bloomberg New Energy Finance report from late last year predicted it as soon as 2025, but Elon thinks that Tesla can do it by 2019, and be less than that in two years. That's a game changer for affordable electric cars, the batteries are the most expensive part, in 2017 they approached the $200/kwh level and that enabled the Model 3 but to get the price to drop 50% in a year is nuts. I get that Elon is usually very optimistic and he's aware of how ballsy his past statements, so I hope he's making more realistic predictions now.

Short term he's predicting that 5000 Model 3/ week by the end of the month is very likely.

Tesla on Monday reported how many cars it made in the final week of the second quarter: 5,031 Model 3 sedans, as well as 1,913 Model S sedans and Model X sport-utility vehicles.

. . .

About 20% of the Model 3s manufactured to achieve the 5,000-per-week target were made on a general assembly line hastily put together beneath a tent outside of its Fremont, Calif., factory in the final weeks of the quarter.

Deliveries of Tesla vehicles, however, failed to meet analyst expectations during the quarter.

During the three-month period, Tesla delivered 18,440 Model 3s to customers globally, the company said. That fell short of analysts’ expectations of 28,000 deliveries, according to a survey by FactSet.

Sales of the Model S sedan and Model X sport-utility vehicle, which typically sell for about $100,000 each, rose slightly to 22,300 combined from 22,000 a year earlier. Analysts had expected a slight increase to 22,500 vehicles.

Tesla�s Engineering Chief Is Out After Taking Leave of Absence

Doug Field�s departure is latest of several high-level executive exits in the last two years

July 2, 2018 7:02 p.m. ET

Tesla Inc.�s engineering chief won�t return from his leave of absence, a person familiar with the situation said, as the auto maker heads into a pivotal period to prove it can sustain production of the Model 3 sedan.

Doug Field, who had been senior vice president of engineering, stepped away from his work overseeing product development at the Silicon Valley auto maker in early May. At the time, a Tesla spokesman said, �Doug is just taking some time off to recharge and spend time with his family. He has not left Tesla.�

People familiar with the move believed at the time he would return six weeks later, but he hadn�t. His departure is one of several high-level executive exits over the past two years as Tesla has struggled to bring out the Model 3, which is priced lower than its other luxury vehicles as part of a plan to transform the company into a more mainstream auto maker.

Tesla on Monday said it met its long-delayed goal of building 5,000 Model 3 cars a week, and that it aims to increase the output to 6,000 a week by late August.

Beyond ramping up Model 3 production, Tesla is racing to develop a slew of new products, including the Model Y compact sport-utility vehicle that Chief Executive Elon Musk has said he wants to unveil in March and begin production in the first half of 2020.

The auto maker confirmed the departure in a statement on Monday. �After almost five years at Tesla, Doug Field is moving on,� the statement said. �We�d like to thank Doug for his hard work over the years and for everything he has done for Tesla.�

Mr. Field couldn�t be reached for comment.

A key leader at Tesla since joining in 2013 from Apple Inc., Mr. Field oversaw the engineering of the company�s vehicles and last year was given oversight of production until Mr. Musk resumed that role last spring.

Mr. Field is credited for helping make the Model 3 easier to build by simplifying engineering complexity that plagued previous vehicles.

At least 50 vice presidents or higher-ranking executives have departed over the past 24 months, according to people familiar with the company, partly because of its acquisition of SolarCity Corp. Mr. Musk sees executive turnover as being in line with other large companies and has announced plans for a management reorganization aimed at flattening the layers of managers.

The Model 3 is a supremely important product for the future of Tesla. It�s what CEO Elon Musk says will help the company get out of the red, and it could also be the first widely adopted all-electric car. And on the eve of one of the most important deadlines in the company�s 15-year history, the company is still figuring out the best way to build it.

Today marks the end of the second financial quarter of 2018, and it�s also the deadline that Musk set for Tesla to make Model 3s at a rate of 5,000 per week. Tesla needs to reach this rate of production so that it stops losing money on every Model 3 it makes. Once it reaches this rate, the company can climb toward the eventual goal of bringing in a 25 percent margin on each of the sedans.

. . . .

The tours could be seen as a small olive branch to the media, which Musk often criticizes, or simply an effort to show the world (including analysts and investors) �everything�s under control, situation normal� ahead of the end of the quarter. Whatever the reason for the access, though, details in both pieces show that � even after Tesla manufactured and shipped tens of thousands of Model 3s to customers since production began almost a year ago � the company is still changing the way it makes its most important car.

Those changes can be big, like the new tent-covered assembly line that Tesla recently constructed in one of its parking lots at the Fremont, California factory. But they�re often much smaller, like the spot welds that hold the car�s frame together, for example. According to the Times, Tesla executives approved an idea from the company�s engineers to have robots make about 300 fewer �unnecessary� welds in order to save time on production.

That Tesla is still making changes to the way the Model 3 is built after some 30,000 have rolled off the line is emblematic of how the company operates differently compared to other automakers. At Ford, or GM, or Mercedes-Benz, decisions like these are often made during the prototyping phase, and the results of those choices are sussed out via rigorous testing long before cars wind up in the hands of customers.

It�s a daring choice for a company that has had issues with quality control. And results from changes made now might not surface until thousands more Model 3s are on the road, well past the moment where we know if the company hit Musk�s marks.

08-02-2017, 03:49 PM

08-02-2017, 03:49 PM

$255.84: -$23.34 (-8.36%)

$255.84: -$23.34 (-8.36%)

{kind=link}

{kind=link}

{kind=link}